Trust, Communication, and the Science of Well-Being

Blog

For decades, non-governmental organizations have ranked corporations in terms of their environmental responsibility. Now, corporations are turning the tables and ranking NGOs for their integrity, effectiveness, and overall level of influence.

The GreenBiz Group, based in Oakland California just released a fascinating report that assess NGO performance based on feedback from over 200 companies. Whereas in the past, NGOs influenced corporate behavior through intimidation and negative publicity, today these organizations are becoming essential partners with the companies they once bullied. The survey’s purpose is to educate NGOs on the type of partnership companies seek.

According to the press release, companies were asked to categorize NGOs into one of four groups:

Trusted Partners – Corporate-friendly, highly credible, long-term partners with easy-to-find public success stories

Useful Resources – Highly credible organizations known for creating helpful frameworks and services for corporate partners

Brand Challenged – Credible, but not influential, organizations

The Uninvited – Less broadly known groups, or those viewed more as critics than partners

This new framework for NGO-corporate alliances is yet another example of the how groups are forging relationships based on trust. Whereas in the past, companies and groups defined their relationships through hierarchy and control, today these models being replaced by trust-based networks.

In a networked environment, such as the emergent NGO-corporate model, relationships depend on influence and cooperation. These principles are built on trust, which requires understanding – not fear and intimidation. In order to get things done, participants must work together by choice. And it’s clear from the framework above that companies aspire to elevate NGO relationships to the level of “partner.”

Surprisingly, only three NGOs achieved the highest rating of Trusted Partner. This tells us that the majority of NGOs have not yet developed internal cultures and service models that enable them to perform as a partner.

The very notion that companies want activists to consider themselves as partners and to aspire to these behaviors, reflects a seismic shift in this once highly contentious field. Instead of denying responsibility for the environment, companies are looking to forge lasting relationships with high-performing external experts.

However, NGOs are quickly learning that partnership requires two-way communication and alignment of goals and objectives. Gone are the days when NGOs can just reach for the nearest bullhorn to get their message out. Today, they must learn how to build more transparent, effective, and agile organizations that seek to fortify trust with their corporate partners. Like many organizations trying to make this shift from fear-based control to trust-based partnerships, the majority of NGOs will need to rebuild their culture from the ground up.

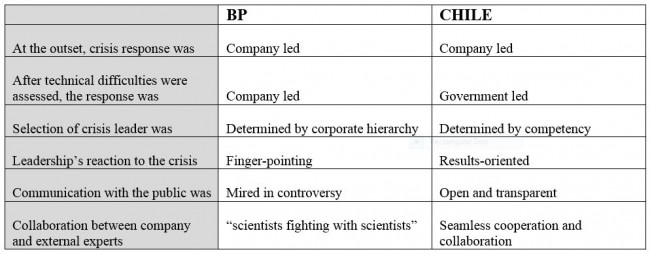

Over the past several years, I’ve studied the role of trust in massive social and environmental crises and two remarkable events stand out from the pack: the BP Oil Spill (Deepwater Horizon) and the Chilean Mine Rescue.

By comparing these events, it’s easy to see how corporate culture influences crisis management. Moreover because the crises occurred in different hemispheres and required the help of experts from a variety of different backgrounds, their comparison illuminates the role of culture more broadly.

In fact, social norms affect how citizens, companies, and governments organize to solve some of the most daunting humanitarian and environmental crises on our planet. Comparing these two specific events reveals how in the U.S. and more specifically–inside BP’s corporate hierarchy, culture clearly hindered progress. However in Chile, culture enabled one of the most successful rescue missions ever.

Culture in the Spotlight

During times of great turbulence, the truth often rises to the surface. Extreme stress drives people and organizations into a state of decision-making that Nobel laureate Daniel Kahneman refers to as “System One,” in his book Thinking Fast and Slow. This impulsive and emotional state of decision-making is common when people are under stress, lacking sleep, and anxious. Therefore, the things people do and say everyday, their habits or automatic reactions, take over. And in poor ethics and values cultures , these default behaviors are not suitable for public scrutiny.

In many respects, Tony Hayward, BP’s former CEO, is now an iconic example of how unhealthy cultures produce incapable leaders. John Bell, the former CEO of Jacobs Suchard, which is now part of Kraft Foods, adeptly describes Mr. Hayward’s failures on his blog:

The entire world was touched by the most environmentally destructive crisis of all time – BP’s oil spill in the Gulf. Everyone watched as CEO Tony Hayward made blunder after blunder while BP’s crude killed. Three weeks after the explosion, Hayward called the spill “relatively tiny” in comparison with the size of the ocean – 6 weeks later he said he’d like his life back, and 6 weeks after that, BP’s shell-shocked Board finally put him out of his misery.

As details emerged in the months and years following the incident, it became clear that Mr. Haward’s actions reflected the company’s culture at the time. It was later revealed that BP had never created an actual crisis management plan for the rig. During the drilling, managers had ignored warning signals, preferring instead to stay on schedule. And, Transocean later claimed that BP intentionally concealed the rate of oil flowing from the Macando well during the first months of the spill. These are all examples of culture. As Elizabeth Hass Edersheim described in the Harvard Business Review:

Culture is an organization’s operating system, the values that everyone lives by. In the case of BP, the culture didn’t work effectively and now its failure is on full display.”

Quite remarkably, it’s the positive side of culture that made the Chilean Mine Rescue such a triumphant success. Whereas BP sought to control information and scientific discovery during the crisis, the Chilean Mine Rescue benefited from specialists and technology from around the world. Through a masterfully coordinated effort, the relatively poor and technically inferior nation succeeded in saving all 33 men in almost 20 days less time than it took BP to shut down the Macando well.

Commonalities between BP and Chile

At first glance, these events seem to have little in common, but when you dig a little deeper, some fascinating insights emerge. Both events occurred in environments where businesses have little or no experience solving problems: thousands of feet under water and rock. Successful leadership depended on deep technical expertise and on-the-spot innovations, including the development of new technology. And, as Mr. Bell referenced above, both events were watched by the world.

While one was an environmental crisis and the other a humanitarian crisis, both directly resulted from business actions. This is an important distinction from natural disasters, which tend to elicit greater levels of sympathy and contribution from businesses and civic groups. A man-made event, however, is often steeped in resentment and anger, at least here in the U.S.

Cultural differences have enormous influence

The differences between how these crisis responses were orchestrated are compelling. With the BP disaster, research reveals constant argument and battles for control between business, government, and technical experts. According to a report from Scientific American:

Scientist fought scientist in the battle over whether to proceed with an established way to plug the leak, the so-called “top kill” operation. Nobel Prize winning physicist and U.S. Secretary of Energy Steven Chu remained unconvinced of BP’s technical case, whereas geologist by training Tony Hayward, CEO of the British oil major, felt it had as much as a 70 percent chance of success.

By contrast, the Chilean rescue effort benefited from an almost seamless coordination of effort between specialists, including NASA and drilling experts from a dozen or so countries. From the outset, the country’s newly elected president, Sebastian Pinera assumed control of the rescue and assembled a leadership team of experts from several different companies. Andre Sougarret, a mining engineer with crisis experience was handpicked to lead the rescue.

Three Harvard researchers: Faaiza Rashid, Amy C. Edmondson, and Herman B. Leonard published a case study called: “Leadership Lessons from the Chilean Mine Rescue,” which details Mr. Sougarret’s remarkable leadership techniques and his ability to balance technical knowledge with collaborative and empowering team-building. His adept leadership skills almost certainly are responsible for the miners’ safe passage to the surface after 68 grueling days underground.

The Chilean rescue effort

As many as three different teams drilled at the same time, using different technologies and different tactics. These were known as plans A, B, and C.

The teams sought technical knowledge and ideas from organizations such as the United Parcel Service and the Chilean Navy.

The teams also welcomed help from those that offered it, such as Maptek, an Australian 3-D mapping software company.

Mr. Sougarret “created a psychologically safe environment, never blaming anyone and always focusing on the learning generated by failure.”

Innovation occurred frequently, experimentation was welcomed, and learnings were quickly absorbed by the full team.

One of the most remarkable aspects of the HBR case study by Rashid et al. is their focus on iterative decision-making. In the U.S. very few organizational cultures are accepting of iterative design and implementation processes. The basic structure of organizations is not conducive to this level of agility. Ms. Rashid and her team explain this clearly,

It isn’t easy for leaders to make the shift to an iterative process; most cultures and systems will stifle their attempts. . . Executives will have to shed the deeply embedded beliefs that important business challenges and opportunities are well defined.

The essence of trust communication can be demonstrated through this well-known and often undervalued assessment process. In any enterprise, three basic principles guide all planning and strategy discussions: To know where you have been, where you are going, and how you will get there. Despite their modest tone and unsophisticated style, these questions drive an assessment process that generates meaningful insight.

Here, these three questions are applied to the current environment in which all organizations compete. To win the hearts and minds of customers, and to fully engage employees, business leaders must stay keenly aware of the larger trends that shape consumers’ mindsets, defining consumer values and expectations of any product or service.

Assessing the consumer mindset

Where have we been?

Complete societal breakdown of trust. Most recently, the disintegration of trust dates back to events occurring after Lehman Brothers fell in 2008. Though, it’s fair to look a little further back and include Enron, Tyco, and WorldCom in this assessment.

Where are we going?

Restoration of consumer trust.Although many American businesses act with integrity, they are unfortunate victims of the current state of mistrust. Even companies with long histories of trustworthiness can easily arouse suspicion today. The prevailing consumer mindset is one that expects to be disappointed with any service or company, and that sets a high barrier for businesses to overcome.Lack of leadership and decisiveness in Washington, DC only increases uncertainty and fear, which foster mistrust.

How will we get there?

Communication. Restoring trust is more difficult than building trust. And, the only mechanism for achieving either of these goals is communication. Just like these three questions, communication is too easily forgotten until it’s desperately needed. When someone notices that fear is seeping in, they reach for that one skill they forgot to sharpen: communication.Here, Goldman Sachs provides a prominent example. The same company that once spared no time for connecting with average consumers now invests heavily in communication. Read more on this story from www.forbes.com.

Trust communication is important today specifically because it solves a critical business problem. Only a few years ago, a crisis of confidence threatened the financial system. Today, it is a crisis of trust that stymies the economy. The only remedy for mistrust is communication.

This page is your reference guide for learning about trust leadership and trust communication in today’s uncertain economic environment. Following are web-based reference materials that inform some of the strategies and theories described on this website. Ultimately, leaders will want to understand the root of these issues. Here, I make that possible.

Currently, this resource is divided into three sections: Leading with trust, Communicating trust, and Identifying trust and mistrust as societal trends. Please suggest new topics for addition to this list via Twitter or Google+.

Section 1: Leading with trust

Building Trust in Business 2012, How top companies leverage trust, leadership, and collaboration.

Not surprisingly, this report was first produced in 2009, the same year that mistrust became a powerful wedge between business and consumers. With only three years of data, the trends identified have limited value but the scope of work, including a survey of over 440 leaders at more than 300 companies, is valuable.

“In 2012, the biggest decline in trust is in leadership – people are noting a lack of consistency, predictability, and transparency in leaders’ decisions and actions. This is a real wake-up call to leaders. It’s a communication issue for sure, and it’s also an issue of involving employees at the right level,” says Linda Stewart, President and CEO, Interaction Associates.

Trust in the Age of Transparency, Harvard Business Review, July-August 2012

The author, Julia Kirby, takes note of the rise in publications designed to help businesses fight the tide of societal mistrust. Her article focuses on the role of transparency as a necessary practice for establishing trust. However, she applies transparency to sensitive aspects of business operations, thereby showing the competitive disadvantages to a trust-based strategy. Kirby also offers a few interesting observations that reveal why it’s so difficult for all of us to wrap our arms around the issue of trust. Specifically, she highlights a widespread sense of vulnerability among Americans that heightens anxiety.

“The real problem might be that, as time goes on, consumers are increasingly being placed in situations where they are forced to trust—and they resent that,” says Kirby.

Building corporate culture, Jack Welch appearing on CNBC’s Squawk Box, March 28, 2012

When asked about the corporate culture at Goldman Sachs in the wake of Greg Smith’s NY Times Op-ed, Jack Welch responded with leadership advice for building a sustainable culture through trust.

“There are people who did bad things there, obviously. The kid didn’t make it up. There are some people who got away with doing bad things. Go in and hang those people… Public hanging is an awful expression but it is what leadership is about in teaching others what we will tolerate and what we won’t tolerate…Public hangings are teaching moments that every company has to do. And it’s worth a thousand CEO speeches.”

Welch’s point about the importance of action as a demonstration of a company’s values reflects the principle that trust is predominantly established through non-verbal communication. If leaders want to create a climate of trust inside the organization, they have to communicate through decisions and actions, not messaging strategies.

Stephen Covey’s lessons on empathetic listening, inspiring trust, and relationship-based communication strategies will continue to be wellsprings of insight for years, if not decades. He was a pioneer in many of these areas and remains an authoritative expert through the instructions and advice he left behind. As we see in the emergent Trust Economy, the very issues Covey identified long ago: empathy, emotions, relationships, and trust, are converging and thereby becoming more influential in the marketplace. Following are a few of his notable statements on these topics.

“The first [leadership imperative] is to inspire trust. You build relationships of trust through both your character and competence and you also extend trust to others. You show others that you believe in their capacity to live up to certain expectations, to deliver on promises, and to achieve clarity on key goals.”

“The High Cost of Low Trust: Most organizations have no clue of the enormous cost of low trust, and because most executives have no means of measuring its bottom-line impact, they have little motivation to seriously address it.”

“When I say empathic listening, I am not referring to the techniques of “active” listening or “reflective” listening, which basically involve mimicking what another person says… I mean listening with intent to understand… It’s an entirely different paradigm. Empathic (from empathy) listening gets inside another person’s frame of reference.”

There are too many sources to gather them all. These are just a few:

Then, of course, there’s the book Stephen Covey published over 20 years ago: The Seven Habits of Highly Effective People, which remains a great resource for leaders who seek to build trust.

Psychological Foundations of Trust, Jeffrey A. Simpson, Association for Psychological Science, 2007

To build trust, we’ve always been taught to focus on actions, not words. In business, several things complicate that simple axiom. First, business schools don’t teach trust, they teach competence. Second, companies are not organized around trust; they are organized around the functions of business. Therefore, the functional department of communications is often tasked with upholding trust. Consequently, business leaders and their employees develop communication strategies as a means of establishing trust.

Underpinning these misconceptions about trust is the surprising lack of research that exists on the topic. In this paper, Simpson provides a survey of published research on the topic of trust spanning over four decades. The results are astonishingly meager when contrasted with the subject’s significance.

“Trust lies at the foundation of nearly all major theories of interpersonal relationships. Despite its great theoretical importance, a limited amount of research has examined how and why trust develops, is maintained, and occasionally unravels in relationships.”

“Trust involves the juxtaposition of people’s loftiest hopes and aspirations with their deepest worries and fears.”

Section 3: Identifying trust and mistrust as societal trends

The Trust Deficit, Jon Huntsman appearing on The Colbert Report, August 30, 2012

Huntsman, whose bio includes serving as ambassador to China, serving as Governor of Utah, and most recently running for The Office of President of the US, attributes the current epidemic of societal mistrust to the actions of our elected officials and their apparent lack of honesty. He identified systemic issues such as term limits (for congress), campaign finance, and the revolving door between DC-based lobbies and Congress.

“Why do we have a trust deficit in this country?…Because we’re not getting the straight scoop from our elected officials. And because of that, people don’t trust their elected officials, they don’t trust their institutions of power.”

Trusting and Being Trusted in the Sharing Economy, Forbes Magazine, May 2, 2012

Hailed as the latest solution to our sluggish economy, the concept of Collaborative Consumption isn’t as offbeat as it initially sounds. The movement is supported by real financial transactions and investments. Although the numbers are not sufficiently compelling to justify a term like The Sharing Economy, there is a substantial societal trend away from ownership. And, this trend has just begun to show its long-term capability to change commerce as we know it today. Naturally, a business model based on sharing relies on trust and this Forbes article highlights how precarious and misunderstood trust really is.

“People talk very inaccurately about trust as if it were a unitary thing. It is not. ‘Trust’ is the result of a trustor and a trustee arriving at an agreement. The two parties are not doing the same thing. Trust is an asymmetric relationship.”

Steve Case and Rachel Botsman, the two most prolific voices of Collaborative Consumption, frequently highlight the criticality of trust in this new model which begs the question: If trust is so important, why not call it The Trust Economy?

More resources will be added to this list over time. Again, please contact me to make any suggestions.

Thank you.

Why does your business need audience centric communication? In short, because no one believes the things companies say, any longer. Words have lost their power to persuade in these days of cynicism and distrust. Regardless of the size of your marketing department and the amount of your advertising budget, it is not possible to influence trust or increase likeability by talking about your product or service.

The brand called trust

Once upon a time, companies made products that exceeded customer expectations largely because the products also exceeded customers’ imaginations. This not-so-mythical period was in the 1960s and 1970s when “innovative” was used to describe products ranging from laundry detergent to cars with anti-lock brakes.

Imagine for a moment, a young couple in 1975, buying a new car for their family. They arrive at the dealership thinking of station wagons with room for little Jimmy’s crib in the back. Then, the salesman tells them about the car’s brand new anti-lock braking system. Now, ask yourself if the young mom and dad haggled with the salesman over price.

When products “wow” us, they reach us emotionally, and we buy them. Moreover, when a product offers us something we never imagined owning, we feel almost grateful to have it. Little Jimmy’s mom and dad felt grateful to buy that car, with its remarkable innovation that made driving safer. What a great company, what a great product. What a great time to work in advertising.

Today, the demands of customers are different and the brand they seek is called trust. Marketing gimmicks with clever advertising slogans are almost useless. Even the iPhone, a product that surely “wows,” is subject to this undercurrent, and so far, Apple is upholding trust through its personable retail model and product reliability.

Understanding Audience centric communication

Unlike customer-centric communication, which ostensibly begin and end with the customer in mind, audience centricity comprises customers and employees. After all, employees are the representation of a company’s brand and values. The way an employee projects these values determines customer perception, and no amount of advertising can override real customer experiences.

When companies make a change to their business, they develop a minimum of two distinct communication strategies: one for internal audiences and one for external audiences, or customers. The vast majority of companies, however, develop many communication strategies based on the number of marketing and communication departments. These may include Public Relations, Internal Communications, Shareholder Communications, Customer Marketing, and Prospect Marketing, to name just a few. Depending on how decentralized a company is, there may be even more independent teams working to develop independent communication strategies.

Clearly, this process is inefficient and wasteful. The employee hours devoted to these tasks is staggering when accounting for the writing teams, proofreaders, designers, and publishing teams assigned to each project. Equally concerning is the excess risk incurred through these independent processes. The risks of inconsistency and quality deterioration are simply unnecessary. Surprisingly, however, this is how communications function in most organizations today.

Audience centric communication, conversely, is a methodology that develops a single strategy for all audience segments, while allowing for regional and segmentation-based message customization. The overall strategy, however, applies to all audiences, including employees. This is a critical difference. In order for employees to effectively represent a company to its customers, they have to understand change from the customer’s point of view. Changes, therefore, are contextualized from a customer standpoint in a way that enables employees to uphold customer confidence.

Because the process assesses all audience segments simultaneously, it ensures brand integrity, message quality, and message consistency. Additionally, the initial assessment allows communication leaders to flesh out pivotal decisions that can influence trust and loyalty. Consequently, the communication does more than deliver information; it engenders goodwill while strengthening the ties between employees and the customers they work for.

“Mirroring” Customers

Harris interactive, the market research and consulting firm, has its own take on audience centricity. The company advocates “mirroring,” a strategy that seeks to align employees with customers through communication. This approach is intended to improve employee responsiveness to and anticipation of customer needs. Find out more atwww.harrisinteractive.com or read the PDF here.

Harris Interactive’s research also validates the importance of trust-based communication: “We’ve frequently found that customers consider the emotional, relationship-based aspects of value delivery—trust, communication, interactive/collaborative components of service, anticipation of needs, brand equity, etc—much more important, and more leveraging of behavior, than the functional aspects.” This quote comes from a 2008 Harris Interactive Executive Brief called: Profitably Linking Employee Behavior to Customer Loyalty: Driving Customer Commitment Through Employee Attitudes and Actions.

How trust is changing business communication

Back in the 1960s and 1970s, the way companies communicated with customers was revolutionized. Instead of telling customers about every feature of their products and services, advertisers learned the power of simple and shaved company messages down to brief, tantalizing messages. Leo Burnett, the pioneering advertising executive from that era summarized the values of the day in this directive to aspiring marketers: “Make it simple. Make it memorable. Make it inviting to look at. Make it fun.”

Burnett’s 1960s credo still has tremendous value today. The power of simple will always reign over complex and confusing. However, consumers have become leery of things that look too good to be true. This distrust is well-earned, and after the events of 2008 and 2009, distrust has become deeply woven into the fabric of societal values. In short, people are afraid of being vulnerable.

Consider again Apple’s strategy. The company has an almost captivating image of simplicity that reflects consumers’ desire for clarity in their own lives. However, the company supports this strategy with a remarkable human touch that every prospect and customer can experience via the company’s stores. The product design is still restrained and memorable, but the communication experience is rich, personal, and open to all.

While consumers still desire products that “wow” them, they also want to feel that the company will treat them with respect, after they’ve handed over their hard-earned money. Instead of making a product look “fun” as Burnett once advised, companies would be wise to demonstrate integrity and civility in their customer experience.

Audience centricity is not a stand-in for customer experience management, but it is an outside-in communication methodology that enables companies to build their own brand of trust. Please contact me for more information.

To understand audience centricity, it’s helpful to review recent evolutions in organizational design. Business leadership has evolved significantly, and almost dramatically, in the past half century, fueled by changes in the broader economy. Responding to changes in societal values and customer needs, businesses have changed their internal organizational models. Though, not always for the better.

Product centric vs customer centric

Product centricity is not quite as simple-minded as it now seems. Many customer-centric advocates demonstrate the virtues of their approach by contrasting it with outdated, product-focused models. They argue that to shape a business around its customer segments is the new enlightenment.

For certain, business has learned that putting people ahead of products will often lead to better outcomes. However, Steve Jobs didn’t spend his days and nights sifting through market research and conducting focus groups. He spent his time creating exceptional products, products that people loved.

Great products and services are the offspring of ingenuity and conviction. Extraordinary products and services invoke the kind of passion that employees want to be part of, and customers want to benefit from. That kind of passion is powerful and should be embraced, not quarantined off from the rest of the organization.

Two sides of the same coin

Those who claim that organizations need to be more customer-centric are correct. And, those who claim that organizations need to rally around products are correct, too. Then why are these methodologies treated as mutually exclusive? Why are they compared and contrasted? When customers were neglected by myopic product managers, perhaps the apparent solution was to shift things around.

Shifting them around has created a lot of confusion for employees, and managers, too. Each new organizational design is intended to increase efficiency by increasing role clarity. For employees, however, the confusion only has a new name, a new structure. The tidal pull between customer and product is left resolved. Employees need to be experts on both, at the same time. So, employees on the customer team are no less challenged than their predecessors on the product team. Only the names have changed.

Let’s return and look at the root problem. When myopic product managers undervalued customers, they were actually destroying trust. That same trust relationship with customers is just as important with employees. As Peter Drucker explains below, the real change that occurred is a mindset shift in what we value as a society.

A lesson on organizational trust from Peter Drucker

Organizations are no longer built on force but on trust. The existence of trust between people does not necessarily mean that they like one another. It means that they understand one another. Taking responsibility for relationships is therefore an absolute necessity. It is a duty. Whether one is a member of the organization, a consultant to it, a supplier, or a distributor, one owes that responsibility to all one’s coworkers: those whose work one depends on as well as those who depend on one’s own work.Read Drucker’s full article, Managing Oneself, at www.hbr.org.

Building trust with an audience-centric mindset

Audience Centricity says that responsibility for trust within the organization and with its customers is an absolute necessity. Both audiences are critical.

With each successive corporate failure after Enron’s 2001 collapse, customers and the public-at-large have become overwhelmingly distrustful of business. In addition, our economy’s fundamental drivers have shifted from mass consumerism and the quest for ownership to the desire for experience. Instead of owning a car, they want to rent one for the weekend.

Experience isn’t product-centric, it’s people-centric. While many businesses have embraced the concept of customer centricity, they’ve forgotten that positive customer relationships are not established in the board room. Employees at all levels of an organization define a company’s relationship with its customers. These everyday workers are the voice and face of a company. Companies cannot be customer centric without being employee centric and supporting a thriving relationship between the two.

Apologies are a delicate matter, and the success of an apology can depend more on the type of error than the nature of the confession. People tend to be forgiving of errors caused by lack of experience or inability to perform in a challenging environment. U.C. Davis professors Kimberly Elsbach and Steven Currall say these incompetent acts can be attributed to factors outside a person’s direct control.

In fact, shareholder letters commonly acknowledge mistakes in judgment that affected business performance. These acknowledgements are generally accompanied by an equally candid discussion of lessons learned and improvements implemented.

However, many business mistakes are not caused by incompetency but a lack of integrity. One prevalent reason for error in business is arrogance. When business leaders become overly confident in their own capabilities and start to feel invincible, the risk of hitting an iceberg increases dramatically.

Elsbach and Currall say their research reveals that people are not forgiving of lapses in morality (e.g., arrogance, dishonesty, corruption). Mistakes that reveal a lack of integrity are perceived as permanent character traits, which reveal a dearth of moral fiber.

The Price of Arrogance at Netflix

In 2011, Netflix caused customer outrage when it increased prices by 60% and informed its loyal customers of the changes in a brief, matter-of-fact email. A few months later, 800,000 angry and outspoken customers defected.

The company’s CEO Reed Hastings apologized to customers through video and written blog posts. Today he freely admits that the company’s tremendous success and his own personal arrogance blinded his view of customers’ interests. However a year after Hastings’ candid apologies, the company slid to its lowest stock price. Essentially, the apology was not effective.

The true cost of arrogance has a long tail. Netflix’s stock is enjoying a healthy rebound in 2013, yet Hastings is not celebrating. According to an April 27 New York Times article, Hastings said the company has little room for error, “It’s like a partially healed bone,” he said. “It’s still quite fragile. Were we to make a similar mistake, we’d be right back in the penalty box.”

Alienating traditional customers

JCPenney’s stumble is similar to Netflix’s in that the company’s policies disaffected its core customer base. Traditional customers lived for the emotional high of getting a deal, which eventually became a weekly ritual. When the company suddenly stopped coupons and weekly sales, customers lost their emotional attachment to the store and started shopping elsewhere.

Many stock analysts attribute Ron Johnson’s errors to arrogance. Their analysis frequently cites that Johnson didn’t test these strategies before implementing them at over 1000 retail outlets. Moreover, Johnson’s modern store layout and elimination of weekly sales and promotions were designed to attract a new, more upscale customer base. Remarkably, these weekly promotions were stopped before strategies to attract new customers were ready to roll out.

Other instances of apparent arrogance include the fact that Johnson chose not to relocate to the company’s Texas headquarters and instead commuted by private jet. The most significant sign of arrogance was that traditional customers were alienated before new customers could be enticed. It seemed as if Johnson wasn’t interested in the core customer, which makes many wonder if he had any genuine interest in or respect for the core brand.

The Customer Experience

The effectiveness of JCPenney’s apology depends on the type of error its customers believe the company made. Their perception of these radical changes in pricing and store layout will determine their willingness to give the century-old retailer another try.

On Facebook, the company posted its new commercial on May 1 and as of today has almost 57K likes. The social media campaign goes by the name #jcpListens, and its YouTube commercial shows about one million views. One thing the commercial and campaign can take credit for already is a high level of engagement and awareness.

Stock analysts are influential on Wall Street; however, it’s unlikely that JCPenney’s customers are overly concerned with the company’s CEO. Customers care about their experience with a brand, particularly their emotional experience. When the company changed its pricing strategy, customers experienced an emotional disappointment. How did that disappointment resonate? Basically, did customers interpret the company’s decisions as arrogance or just foolish?

The numbers will tell.

When an event as catastrophic as the financial crisis occurs, it is our responsibility to understand what went wrong. Apart from the process of ascribing blame is the pursuit of knowledge for its own sake: to understand, to learn, and to grow as a society.

The day after Lehman Brothers shuttered its doors, on September 15, 2008, I scoured the Wall Street Journal along with several of my colleagues but found little in the way of explanation about the human errors that dismantled a 158-year old institution.

As is often the case immediately after a crisis, emotions subvert our ability to see things as they are. Our attachment to the past influences how we understand the present. In the days and months following Lehman’s bankruptcy filing, the crisis deepened and further delayed an objective examination of the past.

Nearly five years later, research and insights are coming to the fore that tell us more than what occurred. Now, we are beginning to learn why. These intervening years have created emotional distance from the past, allowing us to observe without passion and seek answers to enduring questions.

Chronicling cultural change on Wall Street

Allan D. Grody is President of Financial InterGroup Holdings Ltd and has over four decades of experience in global finance. Today, he advises financial institutions on a range of issues from risk management to capital restructuring and recently penned his own assessment of the antecedents to the financial crisis entitled, “Risk Adjusting the Culture of Global Finance in the Information Age.”

In the article, Mr. Grody provided a risk-based assessment of cultural and technological changes that influenced many financial institutions from the early 1980s through to the crisis. He then lent the credibility of his personal experience shaping corporate culture in a 150-year old private partnership during those early decades of global growth. As the business grew and expanded, the firm’s senior leaders frequently jetted to foreign lands.

“We became increasingly detached, ever so slowly, from the personal mentoring that was so critical to communicating a culture across decades let alone generations. . . [Thereby devoting] increasingly less time in preserving the culture we had inherited.

“We recognized this change and hired academics and professional educators to teach ethics and imbue our culture, but it wasn’t the same. We weren’t alone. Our clients, great financial institutions steeped in centuries-long vision and values cultures, hired the same outside mentors and tried similar programs.

Mr. Grody explained how Wall Street firms transitioned from private partnerships to public companies, a process that began in the 1970s and culminated notoriously in 1999 when Goldman Sachs, the last prominent holdout, went public.

He referred to the time when partners had their own money tied to the firm’s success as one when senior leaders actively engaged in careful monitoring of everyday business activities. They walked the floors and took keen interest in determining the weekly market view.

“There was a feeling of closeness in the firms back then – a sense of intimacy felt both culturally and physically. The personal mentoring was easier in this environment. Culture was transmitted almost effortlessly. In seeing a transgression, it could easily be remedied.

“Then it began to change, slowly at first, then more rapidly through a volatile mix of partnership pushed by regulation out of its long standing legally permitted monopolistic pricing habits into an increasingly competitive business model.

“Globalization removed the intimacy in which culture is best transmitted. Partners taking their own capital out of the business through a public sale of its shares removed the tie to their best risk control, putting their own money on the line.

“The final nail in the coffin of any semblance of a suitable moral and ethical culture was the anonymity and claims of ‘I didn’t know,’ permitted by the evolving technological complexity.

Increasing the psychological connection to customers

According to Mr. Grody, the winning-at-all-costs mentality that pervaded many financial firms skewed their culture because that type of greed “has no counterpoint in fear.” However, fear of loss can be realized in many ways, including a threat to customers’ wellbeing. Financial firms, and many technically oriented businesses for that matter, lack a vibrant and compelling correlation between business decisions and human outcomes, essentially the experience and mindset of their customers.

In the average organization, regardless of industry, the majority of employees never meet directly with a customer, a reality that is even more pronounced for technical experts such as financial investors and traders. As a result, the human side of financial decisions rarely penetrates the walls of large financial institutions, creating a risk of apathy.

Mindset segmentation, the process of grouping customers based on their psychological profile, values, and expectations, establishes a human representation of customers within the organization. These mindset-based identities are so lifelike that business leaders can intuitively assess customers’ perceptions of business changes. Mindsets enable employees to empathize with customers’ desires and values, thereby humanizing customers in an otherwise rational and data-driven environment.

According to Art Markman, PhD, Professor of Psychology and Marketing at the University of Texas at Austin, empathy allows us to share other people’s emotions. He says research suggests empathy increases a person’s intrinsic motivation to be helpful and that it is possible to boost a person’s level of empathy.¹

In addition, increasing the psychological and emotional connection to customers has been shown to improve internal communication and collaboration. By transitioning the psychological connection from company to customer, employees become less wedded to their functional departments and more inclined to support integrated goals that emphasize organizational outcomes.²

From a communications standpoint, mindset segmentation is a particularly valuable tool for scenario planning because mindsets are predictive indicators of how people will respond to change. In financial services, identifying customer segments that react more emotionally to market volatility can inform communications planning in advance of a specific event. Through empirical study, this expertise can develop into a new core competency and competitive advantage.

The majority of employees in any organization care about their customers. That empathy can enhance communications and act as a stabilizing mechanism against a winning-at-all-costs mentality.

As Mr. Grody explained, “The culture of the financial services industry is now left to be reengineered in the context of a very complex information technology and communication environment.” To combat these technical complexities, I can’t think of a more powerful counterbalance than the very human and emotional heartbeat of customers.

¹Tobias Greitemeyer, Louisa Pavey, and Paul Sparks. “I Help Because I Want to, Not Because You Tell Me to. Empathy Increases Autonomously Motivated Helping.” Personality and Social Psychology Bulletin. May 2012. Vol. 38 No. 5 681-689.

²Robert J. Fisher, Elliot Maltz, Bernard J. Jaworski. “Enhancing communication between marketing and engineering: The moderating role of relative functional identification.” Journal of Marketing. Vol. 61 54-70. July 1997.

To learn more about mindset segmentation, look for my forthcoming book, “Leading with Trust: How the Financial Crisis Transformed Business,” or contact me directly.

Allan D. Grody, President, Financial InterGroup Holdings Ltd

Mr. Grody has been involved in the financial industry for his entire business career of over four decades. He has been consulting domestically and internationally on strategic issues of governments, regulators and financial institutions. His activities have encompassed countrywide restructuring of capital market regulations in anticipation of pan European competition; strategic planning for the banking sector in the Persian Gulf region after the Gulf war; restructuring of capital markets trading in Italy; a visionary year-long study of the future of banking for the American Bankers Association; and expert witness testimony in a landmark patent case related to the electronic trading of financial instruments.

Early in his career he was involved in innovative technology projects within the banking, securities, investment management and futures sectors of the financial industry. He continued to serve the financial industry as the founding partner of Coopers & Lybrand’s (now PWC’s) financial services consulting practice, and later went on to found businesses in financial planning, trading, risk management and internet based financial services.

Professor Grody founded and taught the only graduate level Risk Management Systems course at NYU’s Stern Graduate Business School. He has served on many trade association committees and is a frequent speaker at industry and government sponsored conferences. He is currently an editorial Board Member of the Journal of Risk Management in Financial Institutions, an advisor to the Financial Stability Board and a Blue Ribbon Panel member of the Professional Risk Management International Association.

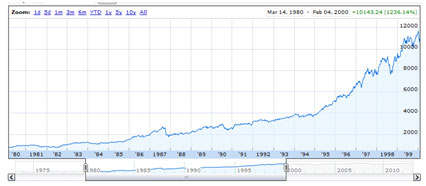

Last week, the Dow Jones Industrial Average (DJIA) set a new record high, closing the day at 14,253.77. Only four years ago this March, the market hit bottom during the financial crisis, closing at 6,547.05. It was the market’s lowest level in twelve years, and those forfeited market gains became known as the lost decade in stocks.

Surprisingly, the fear and trauma of March 2009 is not counterbalanced by euphoria in March 2013. Just three days after the market hit a new high, the U.S. Department of Labor’s monthly jobs report revealed that unemployment had reached a four-year low. Yet these numbers generated relatively little news, which raises an intriguing question: What happened to the hubris of good numbers?

Have Americans become immune to these indicators of prosperity or have we simply lost our penchant for reckless daydreaming? To understand today’s sober response to market gains requires more than an assessment of corporate profits and European instability. Although the financial crisis is four years in the past, the disappointment and disillusionment of that catastrophe has a lasting impact on American culture. By appreciating the human toll of the crisis, we are able to provide meaningful context for today’s events.

As it turns out, the decades of economic growth prior to the financial crisis affected Main Street and Wall Street very differently. While the culture of global finance became increasingly impersonal during this period of roaring market growth, individual investors unknowingly became increasingly vulnerable to a range of technical issues they barely understood. When the crisis hit, those differences led to a widespread sense of distrust.

Part I of this two-part series chronicles regulatory and business changes that shaped how Americans prepare for a financially secure retirement. Part II, to be published next week, illuminates changes to the corporate culture within some global financial firms, what Allan D. Grody refers to as “Culture Gone Awry.”

Part I: How retirement investing became personal

In 1980 Ted Benna, a benefits consultant, discovered a new tax-advantaged savings opportunity in the Internal Revenue Code, Section 401(k). In 1981, the IRS sanctioned this new pre-tax employee retirement savings vehicle and nine companies began implementing these plans that same year. The industry took off quickly and according to the Investment Company Institute, in 2012 more than 50 million Americans held a 401(k) representing an estimated $3.5 trillion in retirement savings.

Two concurrent events influenced rapid adoption of the 401(k). First, in the early 1980s, the stock market began a growth spurt that lasted for two decades and consequently caused many first-time investors to feel capable of amassing a sizeable nest egg through their efforts.

1980 to 2000: Two Decades of Growth

Second, corporate pension plans turned out to be a dismal liability on business’ balance sheets. Companies were unable to fund pensions because their workforces were shrinking which meant that the dependency ratio of retirees to working employees was unsustainable.

Understandably, corporations were eager to transfer this risk and responsibility to individuals. Employees, for their part, felt empowered to invest for their retirements with company contributions and the new portability features of the 401(k) meant they could change jobs without forfeiting their accrued value in a pension plan.

However, in 2008, investors’ do-it-yourself joyride came to a screeching halt. This disillusionment occurred while political and economic leaders grappled with an extremely complex crisis which included opaque solutions (e.g., TARP) and remarkably few criminal indictments. In effect, millions of Americans experienced a deep sense of fear about their own financial futures without a clear sense of culpability. By and large, no one was held directly responsible for their tauma.

In crisis communications, we study the dimensions of fear and develop both messages and tactics that rapidly alleviate fear and restore confidence. Among these tactics are evergreen principles such as transparency, candor, clarity, speed, and empathy. Some of these tactics are applied to messaging, others are applied more strategically. The response to the financial crisis, from business and government left Americans feeling more confused and less confident.

Perhaps the most notable aspect to bear in mind is how personal and emotional these issues are for many Americans. Not too long ago, investing was reserved for those with disposable income. It was an activity for wealthy Americans who wanted to preserve wealth for future generations. Today, however, the most uninformed and uneducated among us are charged with investing for financial security in retirement. Both the players and the rules of the game have shifted markedly.

When the market climbed for over two decades, investing led to hubris because it was not based in fear. As Allan Grody cites from another writer: the culture within banks shifted from “hate to lose” to “love to win.” Individual investors shared that same attitude.

Today, the pendulum has swung the other way.

Part II: How global finance became impersonal Next week, we’ll assess the market influences and business decisions that diminished corporate culture and values prior to the crisis.

As a communication professional who worked in financial services during the crisis, I reflect more on the things we did not say to customers in those dark days than what we did say. While the market fell in 2008, remarkably few voices in the financial industry offered caring and compassionate advice to traumatized investors.

In a heavily regulated industry such as financial services, communications are intricately planned and thoroughly vetted before they reach the public. When Lehman Brothers fell, the industry was dealing with an array of unprecedented issues, among them was the challenge of communicating through a period of prolonged and intense volatility.

As a result, advisors and investment managers said very little when investors felt most vulnerable. This absence of empathy fostered distrust, which continues to hamper the industry four years later. According to Barron’s, investors pulled an estimated 7 billion out of stock mutual funds in 2012, despite a year of relatively stable market performance.

Micro-messages & micro-inequities Communication is commonly understood as something that is said. However, the absence of communication can deliver a far more powerful message. Failure to demonstrate empathy conveys that someone else’s problems are not relevant. That inequality sends a potent message that is not soon forgotten.

Mary P. Rowe, Ph.D., an economist at MIT, coined the term micro-inequity in the 1970s to describe small actions and messages that promote workplace inequality. She defined micro-inequities as: “apparently small events which are often ephemeral and hard-to-prove, events which are covert, often unintentional, frequently unrecognized by the perpetrator, which occur wherever people are perceived to be ‘different.’”

According to Sharon McMillen Cannon, Ph.D., Associate Professor of Management and Corporate Communication at The University of North Carolina at Chapel Hill,

Wherever you observe a difference in power, those in power can send poorly executed behavioral messages to those with less power. During the financial crisis, the messages of people perceived as powerful within financial institutions sent ‘micro-messages’ that created mistrust in the public.

Dr. Rowe’s research on workplace equality at MIT, led to her discovery of micro-inequities and their converse, micro-affirmations. Over the years, researchers have applied these terms to other instances where an imbalance of power exists, such as the doctor/patient relationship and the relationship between doctors and nurses. In the financial crisis, when average Americans felt extremely confused and vulnerable, micro-inequities were pervasive.

Communicate to promote balance

Although an imbalance of power is a consistent component of workplace dynamics, it is an inconsistent component of marketplace dynamics. Depending on the circumstances, customers may feel more or less vulnerable to a business. Therefore, when the balance of power tips to an extreme, businesses must become agile communicators in order to avoid an erosion of trust.

Another important reminder for communicators is that while trust is not established through verbal communications, it can be destroyed verbally. In the spring of 2010, while oil gushed out of the Gulf of Mexico, a particularly inept communicator conveyed the most poignant inequity of recent times when he exclaimed, “I’d like my life back.”

This one comment catapulted Tony Hayward to the top position among corporate villains, where he’ll likely remain in the collective conscious of Americans, and particularly those whose lives were genuinely shattered by his company’s error.

However, Mr. Hayward’s full quote from that day illustrates a slightly different intent.

I’m sorry. We’re sorry for the massive disruption it’s caused their lives. There’s no one who wants this over more than I do. I’d like my life back.

If Mr. Hayward could have omitted the last two sentences, his apology would not have become a historic teaching moment for business leaders. Looking closely at his message, it’s clear that Mr. Hayward tried to identify with those who were suffering. However, he forgot about the imbalance of power; the fact that his life had not been destroyed, it was merely disrupted. Therefore, any message about his own experience was destined to accentuate the imbalance of power and fuel animosity.

Yes, it’s arguable that Mr. Hayward’s statement was not exactly a micro-message, however, it highlights the relevancy of imbalances of power in communication. Essentially, the things we say and don’t say can augment or diminish imbalances in power. Communicators should strive to minimize customers’ and employees’ sense of vulnerability, particularly during a crisis, and should therefore remain vigilant of micro-inequities and the dangerous messages they convey.

Return on community (ROC) is the brainchild of Tony Hsieh [pronounced “Shay”], the CEO of Zappos, and author of Delivering Happiness.

When Mr. Hsieh and his team decided to establish a corporate campus to house the company’s three buildings and provide room to grow, he selected an urban setting instead of an isolated corporate campus. By acquiring the former Las Vegas City Hall and its twelve acres of land, he placed his business in the heart of the city. His ultimate vision is for a campus that influences, and is influenced by, the city around it.

Mr. Hsieh said that instead of an insular approach, he and his team took an NYU approach that seamlessly blends a campus with the city around it. As a former student at NYU’s film program, I can attest that this concept creates an extraordinary learning environment because the classroom setting is supplemented by a thriving, dynamic, and very real urban center.

At $350 million, the company’s commitment to revitalizing downtown Las Vegas is significant. That amount includes $100 million in real estate, $100 million in residential development, $50 million in small businesses, $50 million in education, and $50 million in tech startups through the VegasTech Fund.

A unique vision

To understand Mr. Hsieh’s belief in ROC, it is necessary to first understand his belief in happiness as a business objective. He says that happier employees create a better brand experience, and if he is able to perfect the culture, everything else will fall into place.

Culture is the number one priority of the company. A company’s culture and a company’s brand are really just two sides of the same coin.

In his book Delivering Happiness, Mr. Hsieh illustrates his vision for workplace enjoyment:

To judge whether happiness is good for business, take a look at a few numbers:

Fortune magazine’s list of “100 Best Companies To Work For” ranked Zappos at number 6 in 2011 and number 11 in 2012.

When Amazon bought the company in 2009, it reported $1 billion in annual merchandise sales

Mr. Hsieh’s book, Delivering Happiness, has been translated into 20 languages.

Listening to Mr. Hseih, it is easy to see how his commitment to workplace happiness translates to an open campus that connects employees’ personal lives with their work lives.

I think a lot of companies have the assumption that work has to be unenjoyable. ..That leads to this whole thinking of work/life separation and work/life balance. The implication there is that work must not be fun.

Here, we think of it in terms of work/life integration. At the end of the day, it is just your life.

Quantifying value

This leadership vision that business success hinges on an enjoyable and individually fulfilling culture reflects a strikingly untraditional mindset and management style. Expounding on that concept and applying it to measurement, essentially challenging the accepted notion of ROI as the standard means of assessing value, represents a significant departure from established management practices.

Tim O’Reilly, the founder and CEO of O’Reilly Media, has long challenged traditional notions of quantifying business value. He says it is something he has thought about since reading an article in 1975 called the “Clothesline Paradox,” by Steve Baer.

The thesis is simple: You put your clothes in the dryer, and the energy you use gets measured and counted. You hang your clothes on the clothesline, and it “disappears” from the economy. It struck me that there are a lot of things that we’re dealing with on the Internet that are subject to the Clothesline Paradox. Value is created, but it’s not measured and counted. It’s captured somewhere else in the economy.

From the standpoint of measuring value, Mr. O’Reilly is saying that traditional business metrics are, in some cases, too limiting.

Our accounting doesn’t necessarily match the real world, says Mr. O’Reilly.

Accelerating innovation

Zappos’ vision for reinventing a section of Las Vegas is called The Downtown Project and its mission is to: “help transform Downtown Las Vegas into the most community-focused large city in the world.”

The Downtown Project website describes this investment as a big bet based on three guiding principles: collisions, community, and co-learning, which are designed to accelerate serendipity, learning, productivity, and innovation. This is where Mr. Hsieh may be onto something vital to many businesses in our evolving and uncertain economy.

According to companies that assess workplace engagement, a chief complaint from employees in 2013 is change fatigue. Essentially, companies are struggling to adapt to changes in their marketplace and, therefore, undergo a series of successive organizational realignments. This process is taxing on employees and managers alike.

As a student of the financial crisis and its effects on consumer preferences, this employee perspective does not surprise me. Consumer preferences changed dramatically during the crisis and perception of individual wealth plummeted. As a result, customers today are more interested in experience than ownership, which is not congruent with traditional, high-margin product strategy.

More insular businesses, those whose cultures draw their thinking inward, are less apt to understand the drivers of economic change. Consequently, these organizations are adapting to change slowly and painfully through a series of reorganizations that leave managers feeling as confused as their teams.

A more outside-in approach, which Zappos community-based culture fosters, can help employees maintain a workplace mindset that is more tuned in to life outside the company. It also enhances their ability to innovate and adapt in step with consumers. Zappos’ principles of collisions, community, and co-learning can in fact accelerate innovation, learning, and productivity. And, it may just be the ideal business model for coping with uncertainty.

Many businesses are reaping rewards from similar, sustainable business practices commonly attributed to the Sharing Economy. A prime example is AirBnB, a company that launched in 2007 and in 2012 claimed to have booked more rooms than the Hilton hotel chain.

What do you think?

Is Zappos’ new corporate campus a vision other companies should emulate or is it just a risky bet from a well-intentioned CEO? The potential benefits to culture and innovation seem clear, however, do they justify a $350 million initial investment in a city, which ostensibly should be supported by its tax base?

There’s more to this story,and I’m curious to know the opinions of my readers. Let’s hear your thoughts.

This phrase became a company motto at O’Reilly Media in 2008, largely in response to the tremendous amount of value that left our economy during the financial crisis. Five years later, Tim O’Reilly advocates for this principle every chance he gets while applying it to emergent trends, such as the Sharing Economy.

Since 2011, I’ve been chipping away at my own understanding of trust, particularly from an organizational communication standpoint. After all that I’ve read and studied, however, it seems that the questions still outnumber the answers. Psychological researchers disagree about how to define trust and the business community rarely speaks about it from an evidence-based standpoint.

In short, it is easy to preach the heroic attributes of trust but surprisingly difficult to make a foolproof case for trust in a business context. Therefore, it might be more fruitful to define the ideal productivity experience of a high-trust organization instead of defining trust itself. Create more value than you capture instructs how we make decisions, trustworthy decisions, and it applies to all levels of organizational leadership.

The meaning

When we create more value than we capture, essentially, we focus less on short-term gain and more on the enduring qualities of our work. To me, the most important aspect of this phrase is that it reminds us of what it means to create value. Inside an organization, it’s natural to feel a sense of accomplishment from a well-crafted presentation or a well-executed plan, but did that work truly lead to more value creation for customers and society?

I often hear business leaders express frustration over their employees’ focus on processes and tasks. It’s the looking down instead of looking up that aggravates leaders. Processes are important, sometimes, and tasks are essential, sometimes. But, the context has to be one of meaningful value creation, and individuals need a concrete assessment tool to evaluate and prioritize their activities.

Therefore, the real challenge is to determine whether workplace activities create lasting value for customers or simply achieve short-term gains for an individual, a team, or a department. The second part of this principle clarifies the type of value that is created. Activities that create personal gain are less important than those that produce meaningful benefit to others.

For example, in a one hour team meeting, which tasks should you share with the group? Some of your accomplishments highlight your personal skills, while other activities may produce greater value to the company and its customers. In this scenario, clearly the second set of activities should be given more attention in a team meeting.

Create more value than you capture is an effective decision-making tool for small, everyday activities and for big-picture corporate strategy.In the hands of an employee, this principle can guide improved self-awareness and task prioritization. In the hands of a manager, this principle becomes an effective performance evaluation tool. And in the hands of senior leaders, this principle can serve Mr. OReilly’s larger goals of building business models that strive for more than short-term profits.

The most successful companies treat success as a byproduct of achieving their real goal, which is always something bigger and more important than they are.

Competitive strategy

When Mr. O’Reilly (who probably prefers to be called Tim) talks about this motto, he often references the open source projects that enabled the web to become a remarkable source of value for all of us.

According to Mr. O’Reilly, the early architects of the web were not self-serving. They engineered an environment that would generate value for decades to come. These early innovators and pioneers developed tools for widespread engagement, giving individuals and small businesses a powerful voice.

Here’s how Mr. O’Reilly explains his principle:

Focusing on big goals rather than on making money, and on creating more value than you capture are closely related principles. The first one is a test that applies to those starting something new; the second is the harder test that you must pass in order to create something enduring.

Take Microsoft. They started out with a big goal, “a computer on every desk and in every home,” and for many years unquestionably created more value than they captured. They helped grow the PC industry as a whole; they built a platform that helped many small software vendors to flourish. But over time, they began to capture more value than they created: as the cost of PCs plummeted, hardware vendors had to survive on the slimmest of margins while Microsoft collected monopoly rents; bit by bit, Microsoft consumed its own developer ecosystem by building the features of successful startups into their own products, and using their operating system dominance to crush the early movers. As I’ve written elsewhere, I believe that Microsoft must re-commit itself to big goals beyond its own profitability, and to creating more value than it captures if it is to succeed. (Danny Sullivan wrote a great piece about the strategic relevance of this very idea just last week, Tough Love for Microsoft Search.)

Workplace engagement

When we examine value creation and value capture as distinct activities, it becomes possible to create a new model for workplace engagement. While businesses unquestionably need to clarify and communicate their core culture, mission, and values (beliefs), these attributes are not directly tied to daily business decisions.

A company’s culture and values should guide employee decisions, but in most instances, they cannot instruct decision-making. Mr. O’Reilly’s motto focuses on how decisions are made. Therefore, employees can readily determine whether their decisions will create value for the company’s customers, or conversely, capture value for their personal or team benefit.

This straightforward litmus test is congruent with activities in both service and manufacturing organizations and has the power to influence greater levels of collaboration, innovation, and organizational trust.

Employees who work collaboratively to create value are more likely to consider the long-term interests of their customers. The process is measurable, sustainable, and highly conducive to trust.

By comparing these events, it’s easy to see how corporate culture influences crisis management. Moreover because the crises occurred in different hemispheres and required the help of experts from a variety of different backgrounds, their comparison illuminates the role of culture more broadly.

By comparing these events, it’s easy to see how corporate culture influences crisis management. Moreover because the crises occurred in different hemispheres and required the help of experts from a variety of different backgrounds, their comparison illuminates the role of culture more broadly.